Impact Investing Like a Rockefeller: What Canadian Families Should Know in 2026

- Jan 1, 2015

- 9 min read

Updated: Jun 1

By Arthur Salzer, CFA, CIM | Northland Wealth | May 2026

You may have watched the ESG debate with some combination of frustration and wariness. The label has become a source of political controversy. Funds have been rebranded and scrutinized for greenwashing. If you have been considering whether to build a values-aligned allocation into your portfolio, the last two years have not made that conversation easier.

Here is what the controversy has obscured: impact investing is a different thing entirely. It always was. The families that understood this distinction have continued building disciplined, measured allocations while others retreated. The families that collapsed the two concepts together, or abandoned the effort entirely, have given up a planning tool that serves both their financial objectives and the harder work of keeping the next generation engaged with the family's capital.

Why has ESG investing come under fire, and why does it matter for Canadian families?

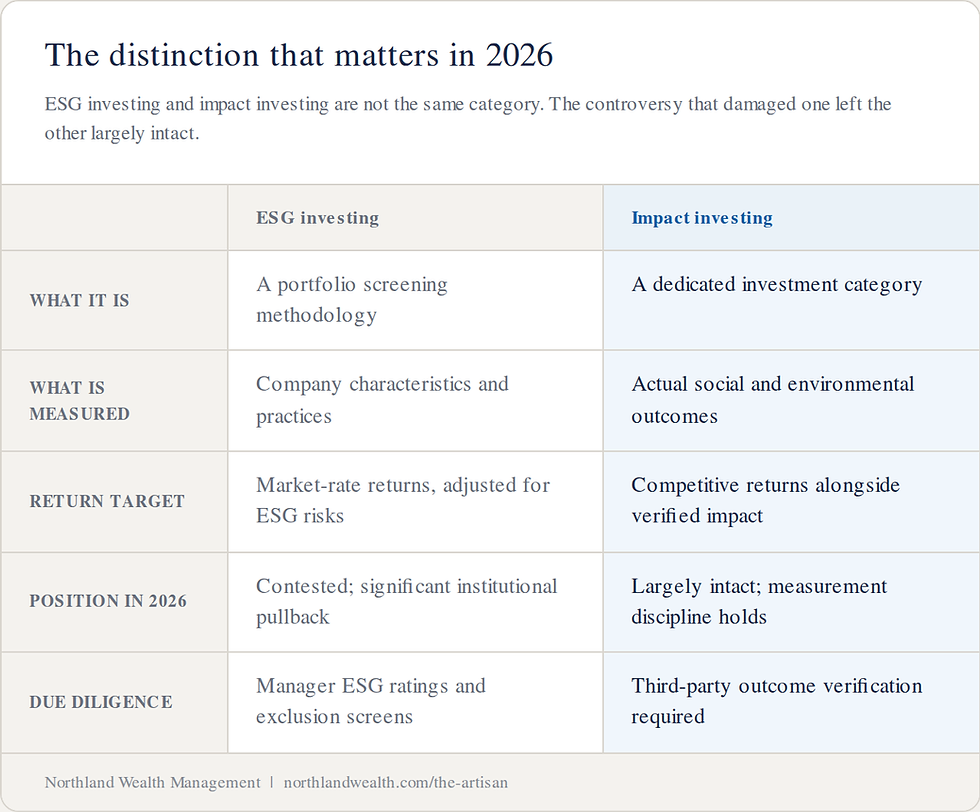

"ESG" and "impact investing" are not the same thing. The distinction matters more in 2026 than it did when these concepts first entered the mainstream.

ESG investing applies environmental, social, and governance criteria as a screen or weighting approach within conventional portfolio construction. You may underweight oil companies, exclude tobacco, or tilt toward firms with strong board diversity. The investment thesis is that ESG factors correlate with long-term risk management. ESG is fundamentally a portfolio construction approach, not an asset category.

Impact investing is something different. It directs capital specifically toward companies, funds, or projects with a measurable positive social or environmental outcome alongside a financial return. The measurement is not optional. It is built into the investment mandate.

The backlash against ESG investing has been real. Across multiple U.S. states, legislation was enacted restricting ESG considerations in pension fund mandates. Major asset managers walked back their public ESG commitments. The pressure has been significant enough that some institutional investors now practice "greenhushing," continuing ESG analysis without publicizing it to avoid controversy.

Impact investing emerged from this period in substantially better shape. Because it requires measurement of actual outcomes rather than adherence to labels, it is harder to dismiss as ideological window dressing. A portfolio manager who can show that a specific investment created 1,200 jobs in underserved communities and produced a 14% IRR has a very different conversation with a sceptic than one who can show an ESG rating improved.

Canada has been less susceptible to the U.S.-driven ESG backlash than some observers expected. The Canadian regulatory environment, pension culture, and family office ethos have been more receptive to values-aligned investing. But the distinction between impact and ESG still matters here, because families deserve to understand what they own and why.

What was the Rockefeller moment that set the standard for impact investing?

In November 2014, Arthur Salzer moderated a panel discussion at the Campden North American Family Office Conference in Boston. The panelists were Justin Rockefeller, co-founder and chair of The ImPact and trustee of the Rockefeller Brothers Fund, and Antonio Ermirio de Moraes Neto, co-founder of Vox Capital in Brazil.

The timing was notable. Weeks earlier, the Rockefeller Brothers Fund, a private foundation established in 1940 by Justin Rockefeller's grandfather and great-uncles, had announced it would divest from fossil fuels. The announcement drew sustained attention because of who was doing the divesting: the Rockefeller fortune originated in Standard Oil, which controlled nearly 90% of U.S. oil production at its peak. Whether you agree with that specific decision or not, the underlying principle was clear. The fund had decided that its investment policy and philanthropic purpose could no longer operate in separate compartments.

The lesson is the process, not the conclusion. A different family, with different values, arrives at a different destination. Many Canadian UHNW families view the energy sector and the communities it sustains as a direct expression of long-term values: energy security, resource stewardship, and regional economic vitality. Northland invests across the full economy, including oil and gas, and has written on why that sector deserves a place in long-term portfolios. Impact investing is not synonymous with any particular sector exclusion. It is a discipline for connecting what a family believes with where its capital goes.

Justin's argument was direct: families that invested on financial criteria alone while giving away on charitable criteria were missing something significant. Not just returns, but relevance. The ability to engage the next generation around shared values, in the domain where the family's actual capital was deployed.

Antonio brought a different dimension to that conversation. His firm, Vox Capital, was directing private equity capital toward companies serving Brazilian households with limited incomes, in healthcare, education, and housing. The purpose was explicit. The measurement was built in. And the returns were competitive.

A decade later, both organizations are still operating. The ImPact has grown to more than 90 prominent families around the world. Vox Capital has built a multi-cycle track record. The conversation those two panelists were having in 2014 was not aspirational. It was prescient.

When Arthur moderated that Campden panel in 2014, impact investing in Canada was a nascent concept. By 2025, Canada's private impact investing market had accumulated $17.7 billion in total target capital, with $4.2 billion raised in 2025 alone, nearly nine times the 2021 figure. Fifty-five new private market impact products launched in 2024, a single-year record. The market has not moved toward impact investing theoretically. It has moved with capital.

Does impact investing require sacrificing financial returns?

The honest answer depends on which part of the market you are evaluating.

Some impact vehicles do accept concessionary returns. Development finance institutions and certain affordable housing funds explicitly offer below-market rates in exchange for social impact. These are deliberate choices and should be evaluated as such. If a family chooses to accept a 4% return on a social housing fund that would otherwise return 8%, that is a values-based decision worth making with clear eyes.

The mainstream of private market impact investing, however, does not accept this trade-off. Impact private equity, impact infrastructure, and impact-oriented private credit compete on returns with conventional alternatives. The managers that have survived more than a decade of development in this field have done so by generating competitive returns alongside measurable impact. Those that relied on the impact label without investment discipline are largely gone.

A useful frame comes from institutional allocators who have been in this space the longest: the discipline required to measure impact outcomes tends to correlate with better operational management. You cannot measure employment outcomes, emissions reductions, or financial inclusion statistics without rigorous data collection and portfolio company engagement. Managers that build those systems often manage their underlying businesses more carefully than those that do not.

None of this guarantees outperformance. Impact investing requires the same due diligence discipline as any alternatives allocation: track record analysis, reference checks, fee structure review, and an honest assessment of exit dynamics. The impact thesis does not substitute for investment process. It is an additional filter, not a replacement for one.

There is one pattern that experienced allocators in this space consistently notice: the managers most worth backing rarely lead with their impact credentials in a first meeting. They lead with their returns history, their loss analysis, and their exit track record. The impact framework emerges when you ask how they select portfolio companies and what they require of management post-investment. That ordering tells you something important about where their priorities actually sit.

What does Canada's impact investing market look like in 2026?

Canada's private impact investing market has matured considerably over the past five years. The Institute for Sustainable Finance at Queen's University and Rally Assets track the market annually in their State of Private Impact Investing in Canada report, and the 2025 data paints a clear picture.

The market reached $17.7 billion in cumulative target capital as of 2025. Target capital in 2025 alone was $4.2 billion, nearly nine times what was raised in 2021. Product launches hit a record 55 in 2024. Climate change mitigation remains the largest theme by capital, having attracted approximately $4.7 billion in cumulative target capital, but the market is expanding meaningfully into affordable housing, healthcare access, and financial inclusion.

The market is still dominated by small-to-mid-sized products in the $10-to-$100 million range. The median product size is approximately $30 million. That has implications for UHNW families seeking meaningful exposure: access to the better managers often comes through family office networks and direct relationships rather than traditional distribution channels. A $30 million fund cannot accommodate a $10 million allocation from a single investor without concentration concerns.

Globally, the impact investing market is estimated at $2.2 trillion in target capital. Canada accounts for a growing but still modest share. The opportunity set continues to expand, particularly in private credit and infrastructure.

How does impact investing serve the next generation of a UHNW family?

Antonio de Moraes Neto was 27 years old when he spoke on that Boston panel in 2014. He was already directing capital toward a specific social objective, with a track record to show for it. The Votorantim family, one of the largest industrial families in Brazil, had a fourth-generation member who was not waiting to inherit the family office. He was building his own.

That is the outcome families want. Not just preservation of wealth, but preservation of engagement. The evidence from families that have successfully transferred wealth across generations consistently points to shared purpose as a more reliable factor in continuity than investment strategy alone. Governance structures, family councils, and constitutions all matter. But they work better when the rising generation sees the family's capital as something worth engaging with rather than something to wait for.

Values-based investing, done with rigour and measured against outcomes, has shown up in those families' success stories. Not because the impact label is compelling in the abstract, but because the specific conversations around impact allocation, where the capital goes and why, give the next generation a seat at the table with real stakes.

This is not a recommendation to allocate simply because the next generation is interested. Interest is not a due diligence standard. A family should not sacrifice portfolio quality to generate engagement. But where the family already has values and themes they care about, building an investment allocation that reflects those themes, rather than keeping investment and values entirely separate, is a conversation worth having.

How does Northland Wealth evaluate impact investments for client families?

Your current investment manager may be doing an excellent job on the conventional portions of your portfolio. The gap is rarely in public markets execution. The gap is in whether the same firm has the infrastructure to source and evaluate private impact managers, the relationships to access better vehicles, and the planning integration to ensure an impact allocation fits coherently within your broader estate, tax, and holdco structure.

When we consider an impact allocation for a client family, we apply the same framework as any alternatives evaluation: the manager's track record, the fee structure, the fund terms, the underlying portfolio, and a realistic assessment of exit dynamics. We add an impact evaluation layer on top: what outcomes does the manager claim to produce, how are those outcomes measured, who verifies the measurement, and what reporting obligations are embedded in the fund documents.

We are direct with families about what impact investing can and cannot do. It cannot substitute for a well-constructed portfolio. It does not guarantee outperformance. And not every family's values translate into a viable investment thesis at the scale that matters for a UHNW portfolio. What impact investing can do, when built with discipline, is make the connection between how a family thinks about the world and how it deploys capital. That process becomes a foundation for genuine family governance conversations, regardless of where the family's values point.

The families for whom impact investing works best in our experience are those who approach it as an allocation within a broader alternatives portfolio, not as a values declaration in portfolio form. The investment discipline comes first. The values alignment is a filter on top of it, not a replacement for it.

When that discipline is in place, the impact allocation does something else: it creates a genuinely interesting conversation with the rising generation. Not because they are being told the family cares about values, but because they can see the capital moving in that direction and participate in evaluating where it goes. That is what Justin Rockefeller was describing in Boston in 2014. A decade on, it is the practice of more than 90 families who have made The ImPact's pledge to align their assets with their values, and a growing number of Canadian families who have enough capital to matter to the managers building these portfolios.

The families that ask these questions early tend to be the ones whose wealth survives the transition from the first generation to the third. When you are ready to explore what a disciplined impact allocation looks like for your family, we are here for that conversation.

Frequently Asked Questions

About the Author

Arthur Salzer, CFA, CIM is the Founder and Chief Executive Officer of Northland Wealth Management. He has advised ultra-high-net-worth Canadian families on investment strategy, portfolio construction, and multi-generational wealth for more than two decades. Arthur moderated the impact investing panel at the Campden North American Family Office Conference in 2014, and writes on macro policy, investment philosophy, and energy and materials for The Artisan.